What do you make of this as an investor in our funds?

By definition, the future is uncertain, but we do know quite a bit about the past in the capital markets. And the historical evidence is unequivocal: You should not let such events control your investment choices.

The question is whether the current situation is so dramatically different that it becomes pointlessly perfunctory to brush it off with a reference to historical figures. The picture is certainly so hazy that a detailed review may be outdated tomorrow. There are, however, grounds for some more general reflections.

Discussing the financial consequences of such a tragic crisis may seem cynical, but that's nevertheless what impacts the value of your funds. We can start by noting that Russia accounts for about 3 per cent of the world economy, measured in purchasing power-adjusted GDP. This figure is inflated by the fact that the Russian price level is relatively low. Measured by GDP in current market prices, which better reflects the volume of international trade, the share falls to 1.7 per cent.

For companies with relations to the Russian market, of course, it may still be devastating. Sanctions will be met with reverse sanctions, and it will not be easier to sell Norwegian salmon there than it has been for the past eight years. Presently, a total of 1-1.5 per cent of the revenues of the portfolio companies in our equity funds go to companies in Russia and Ukraine. Obstacles in Russian-related supply chains can also affect price growth in the West and contribute to stronger inflationary pressures.

The effect on the energy market is the most palpable. With the mothballing of the new gas pipeline from Russia, Nord Stream 2, we will have a tighter energy balance, and with further uncertainty about supply in existing agreements, oil and gas prices may be propped up for years to come. Whereas, in isolation, this is to Norway's advantage, it is negative for the world economy. However, the contractionary effect is significantly weaker than during previous oil crises, simply because oil accounts for a much smaller share of global GDP.

At this point, you are well served by remembering the source of long-term return in securities: not beneficial business conditions, not absence of risk, not particulary good timing. It is down to the fact that the investee companies make money. This is reflected in the return on stocks and bonds in profitable companies.

And should you still be tormented by uncertainty and disquiet, please remember that everything that has happened, and everything we now know about it, is also known by all market participants and probably fully embedded in prices. If you sell your securities now, you are betting that the conflict will be deeper and more extensive than everyone else is estimating. Such a crystal ball is not among our possessions.

Geopolitical unrest always hits markets in the short term. Unless the conflict escalates beyond the present battlefield, however, it is difficult to see really grave economic consequences for countries other than those directly affected. In the post-war period, we have been through many events with greater consequences for the Western economies than those we see now.

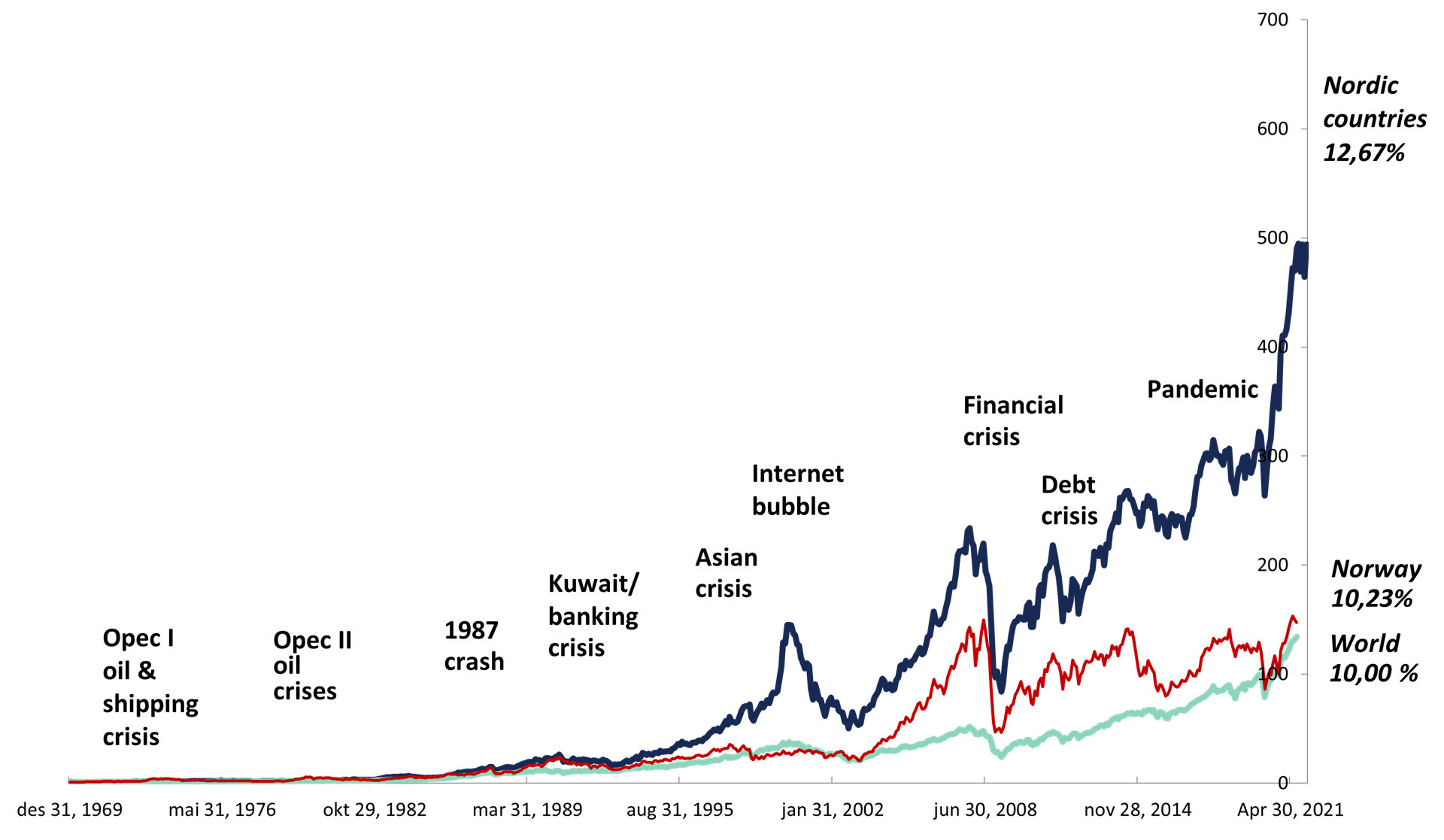

This is clearly illustrated by developments in the Nordic stock market over the last 50 years or so. If, at the beginning of 1970, you invested USD 1 million in Nordic shares, you would now – given considerable patience through every crisis we have experienced – be left with USD 494 million. Such is the cynical reward for participating in business through troubled times.

On top of the world ...

USD 1 million invested in Nordic stocks at the start of 1970 would have grown to USD 494 million today (vs. USD 142 million in the MSCI World Index):