Cloudy rearview mirror

The Optimal Pareto

18.05.2026

A capitalist take on the stock market, earnings and the middle class.

A capitalist take on the stock market, earnings and the middle class.

Worried about the stock market? You may have read that the S&P 500 is priced at more than 40 times earnings. This of course refers to the CAPE (the Cyclically Adjusted Price Earnings multiple), which has only been this high 29 times in monthly data since 1881.

I would argue, however, that if you’re worried about the stock market, this is not what you should be worried about.

First, let’s see why the CAPE is this high. It is based on the last 10 years’ inflation-adjusted earnings, which is all good and fine if earnings move in regular cycles. Now, however, earnings growth has been extraordinary. Over the past 10 years, real S&P 500 earnings have grown by more than 150%, way above the historical median increase of 24%. When you compare present stock prices with much lower earnings 10 years ago, the market is bound to look expensive.

Of course, no investor would now judge a stock by its earnings back in 2016. In terms of forward earnings, the S&P 500 is priced just below 21 – which is spot on the average for the past six years, i.e. after the pandemic. While you may find that expensive, too, it does not scream that you should head for the hills.

Hence, it’s not pricing that you should worry about. It’s earnings.

The key question is why earnings have risen this fast. I’m sticking to the US market here, simply because of its predominance. S&P 500 companies alone make up close to 70% of the MSCI World Index. Do note, though, that earnings have risen sharply also in the STOXX Europe 600 index. This development cannot be brushed aside as a purely cyclical effect.

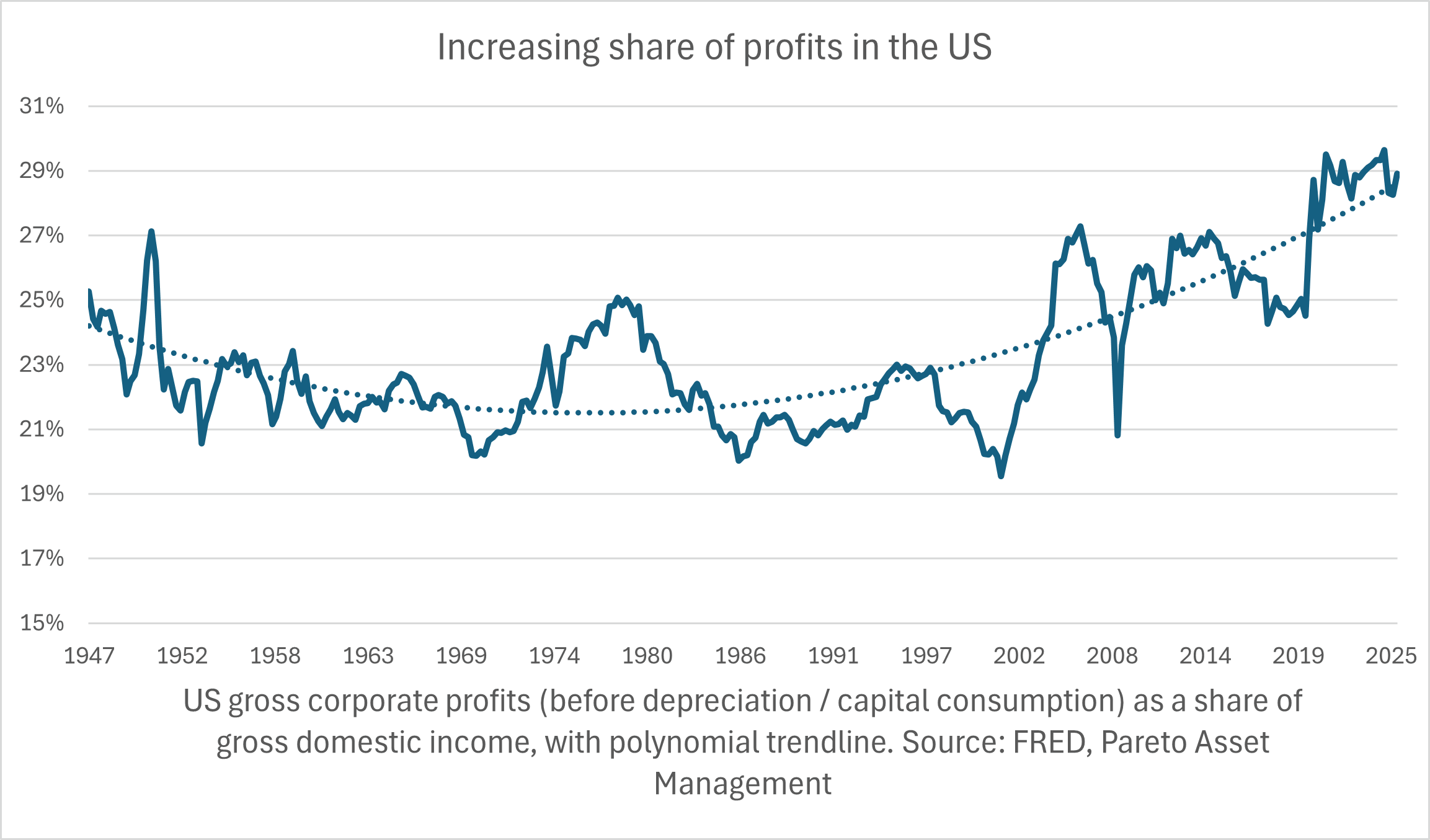

A recurring theme in the US has been the eroding purchasing power of the middle class, due to stagnant wages and salaries. While it now seems that government transfers and other countervailing factors have been underestimated, it is indeed true that the labour share of the US economic pie (before transfers) has been shrinking for decades – from 65% in 1970 to probably below 56% today.

The flip side of this coin, of course, is that the share going to capital has been increasing. Gross corporate profits (including depreciation) in the United States have risen sharply since 1970.

The declining labour share has been attributed to factors like weaker unions and economic policies. In my view, the changing characteristics of industry are no less important. Many of today’s corporate giants have high fixed costs and low marginal costs, which translates to high barriers to entry and lower price pressure. The resulting pricing power lifts profits, while mechanically reducing the labour share.

In other words, if you read about the declining middle class, you may stop to reflect that you yourself, as an investor in these companies, benefit from the same trend. What’s more, you also have a strong reason to believe that much of the increase in profits will not necessarily be reversed.

I’m not saying that present earnings have no cyclical element, and I haven’t even touched upon the AI boom. My argument is simply that changing industry characteristics point to a large part of the increase in profits being of a structural nature.

Hence, the CAPE is not very helpful these days.

About the author

Finn Øystein Bergh joined Pareto in 2010, the first years in Pareto AS before joining Pareto Asset Management in 2015. He has previous experience as a journalist, chief economist and later managing editor in the financial magazine Kapital. Finn Øystein Bergh holds an MSc in Economics and Business Administration, MBA, cand. polit. (an extended master's degree) in political science and cand.polit. in economics. He writes the financial blog Paretos optimale, and has published several books on economics.